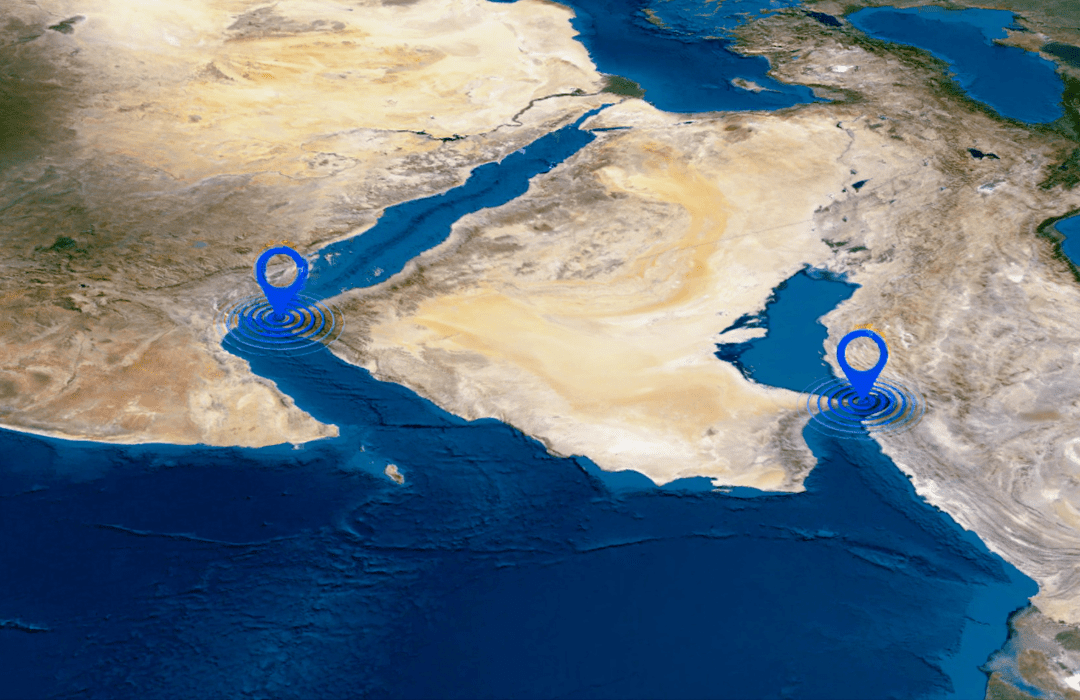

After more than two years of widespread diversions around the Cape of Good Hope, the container shipping industry in 2026 is entering a new but highly uncertain phase.

While some carriers have begun testing or partially reintroducing Suez Canal transits, the latest data shows that a full-scale return has not materialised. Instead, the industry is operating in a hybrid state, with selective transits, cautious carrier strategies, and continued reliance on alternative routes.

This article explores what’s really happening in 2026, which carriers are moving, and what it means for global supply chains.

Why the Suez Canal Still Matters

The Suez Canal remains one of the most strategically important shipping corridors in the world:

- Around 12-15% of global trade passes through the Red Sea-Suez route [suaidglobal.com]

- The route cuts 10-14 days off Asia-Europe transit times compared with the Cape of Good Hope [suaidglobal.com]

- Shorter routes reduce fuel consumption, emissions, and total shipping costs

➡️ Even a partial return can significantly reshape:

- Lead times

- Effective vessel capacity

- Global freight rates

Early 2026: Signs of a Return Begin to Emerge

At the start of 2026, some carriers began cautiously re-entering the Suez corridor.

- Maersk resumed select services through the Suez Canal in early February following successful trial sailings [maritimenews.com]

- Joint services with partners such as Hapag-Lloyd also restarted limited Red Sea transits under naval escort

- Analysts described this as a potential turning point, with phased reinstatement expected over several months if conditions held [maritimenews.com]

At the same time:

- Other carriers, including CMA CGM, tested routes but adjusted plans quickly based on changing risk conditions [maritimenews.com]

➡️ The key takeaway from early 2026:

The industry began testing – but not committing.

Mid‑2026 Reality: Most Traffic Still Avoids the Suez Route

Despite early optimism, the latest updates show that most container traffic is still rerouted via the Cape of Good Hope.

- As of May 2026, major carriers continue to largely avoid the Red Sea corridor due to ongoing security risks

- The majority of Asia-Europe services remain diverted, with longer routing now the “default” operating model

- Transit times are still several days to weeks longer than pre-crisis levels [futureforwarding.com]

Shipping data reinforces this:

- Daily vessel traffic in the southern Red Sea has dropped to around 30-35 ships vs ~70 typically [maritimenews.com]

- Suez Canal volumes, while improving, remain below pre-crisis levels and uneven across sectors

➡️ This confirms that 2026 is not a return to normal – it is a partial recovery with continued disruption.

A Mixed Picture: Recovery Signals vs Ongoing Risk

Positive indicators

- Suez Canal transit volumes stabilised at ~55 ships per day in February 2026, supported by international naval security efforts [ports.marinelink.com]

- The Suez Canal Authority reports:

- +5.8% vessel growth

- +16% tonnage increase

- Ongoing discussions with global carriers about returning

Ongoing challenges

- Red Sea security risks persist, with attacks on commercial vessels still influencing routing decisions [suaidglobal.com]

- Insurance premiums and war-risk classifications remain elevated

- Many carriers continue to treat the region as a high-risk zone requiring constant reassessment

➡️ The result is a split market:

Some services returning cautiously – most still staying away.

The Rise of Hybrid Routing Strategies

One of the biggest developments in 2026 is the emergence of hybrid routing models.

Rather than committing fully to one route, carriers are:

- Using Suez for selected services or urgent cargo

- Maintaining Cape routing for cost-focused or lower-priority flows

- Building flexible networks that can switch quickly based on risk

This reflects a fundamental shift in shipping strategy:

➡️ Routing is no longer fixed – it is dynamic and risk-driven.

Market Impact: Capacity, Rates and Congestion Risk

The gradual reintroduction of Suez routing has significant implications.

Potential Capacity Release

- Returning to shorter routes could release 6–8% of global container capacity [maritimenews.com]

- This is because vessels spend less time at sea, increasing available supply

Freight Rate Pressure

- Capacity release combined with new vessel deliveries could:

– Increase competition

– Put downward pressure on rates

Short-Term Disruption Risk

- A sudden shift back to Suez could create:

– Port congestion

– Overlapping vessel arrivals

– Schedule instability for several weeks

➡️ Any large-scale return could be just as disruptive as the original diversions.

What This Means for Shippers in 2026

Opportunities

- Potential for shorter transit times on select services

- Reduced costs if Suez routing expands

- More routing flexibility

Challenges

- Continued unpredictability in schedules

- Rapid changes in routing decisions

- Ongoing risk premiums and insurance costs

- Capacity swings affecting rates and space availability

➡️ The key for shippers is flexibility – not assumption of stability.

Conclusion: A Transition Phase, Not a Return

The Suez Canal situation in 2026 is best described as a transition, not a recovery.

- Some carriers are returning – cautiously

- Most capacity is still operating via the Cape

- Security risks continue to dictate decisions

The industry is moving toward a more flexible, risk-managed routing model, where:

- Trial transits inform decisions

- Hybrid networks become standard

- Full normalisation remains uncertain

For now, the Suez Canal is back in play – but not yet back to normal.